Why Your Gas Bill, Grocery Prices, and 401(k) All Had the Same Bad Week

Invested In Us | Issue 17 | Week of March 10, 2026

My goodness…what a difference a week makes.

If you read last week’s issue, you know markets were already walking a tightrope. Then the Middle East happened, and the tightrope snapped.

Israel bombed 30 Iranian fuel depots over the weekend. Oil exploded past $100 a barrel on Monday morning before pulling back. The February jobs report came in worse than anyone expected. And the Federal Reserve is now stuck between two options, both of them bad.

We’re going to break all of it down. But first, we have a big announcement.

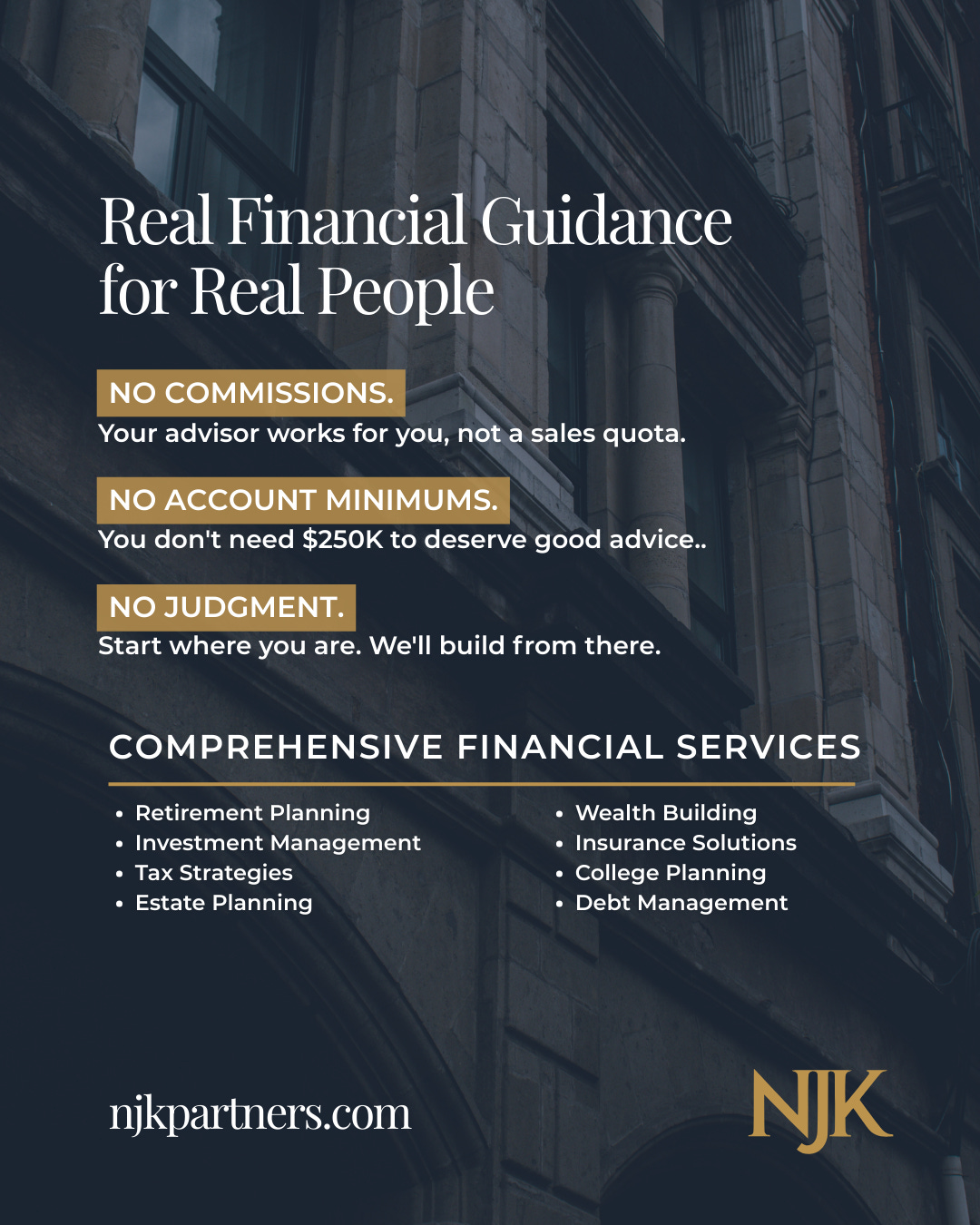

NJK Wealth Management Is Officially Open

This has been a long time coming.

NJK Wealth Management is now officially registered and open for business.

No minimums. No commissions. No cookie-cutter plans.

We built NJK Wealth because we believe everyone deserves access to real, personalized financial guidance, not just people who already have money. The wealth management industry has spent decades telling everyday families they don’t have “enough” to deserve professional advice. We think that’s wrong.

Here’s what that looks like in practice: customized financial plans built around your actual life, your goals, and your family’s future. Your assets will be held with one of the largest and most trusted custodians in the world, and you work directly with us —not a call center, not a chatbot, not an AI advisor.

This is what we’ve been building toward with Invested in Us from the beginning. The newsletter teaches you how money works. NJK Wealth helps you put that knowledge into action.

If you’ve been waiting for a sign to get serious about your financial future, this is it.

State of Capital

Let’s talk about what happened last week, because it was a lot.

The VIX—the market’s “fear gauge”—surged past 35 last week, more than double where it started the year.¹ That tells you investors went from cautious to genuinely nervous almost overnight.

The Dow posted its worst week since April. The Russell 2000 had its worst week since August. Small caps are now down more than 5% on the month. And just a few weeks ago, we were talking about how the Russell 2000 was outperforming the S&P 500.

That’s how fast things can turn.

Small-cap companies are typically the first to feel the pressure when growth concerns show up. They carry more debt, they’re less diversified, and they depend more heavily on the domestic economy. So when investors start worrying about a slowdown, they rotate out of small caps and into larger, more financially stable companies. That rotation happened aggressively last week.

And here’s the thing—despite all the turmoil, the S&P 500 is still trading at roughly 21x forward earnings.² That’s historically expensive for an environment where geopolitical risk is escalating, inflation is threatening to come back, and interest rates haven’t come down. The market is essentially betting that corporate earnings will keep growing fast enough to justify the price tag.

That’s a real bet. And this week will tell us a lot about whether it pays off.

Policy & Economics

The Strait of Hormuz Is Back in the Headlines

If you’ve never heard of the Strait of Hormuz, you’re about to hear about it a lot.

It’s a narrow waterway between Iran and the Arabian Peninsula, and roughly 20% of the world’s oil supply passes through it every day.⁵ In some areas, the shipping lane is only about two miles wide. It is, by almost any measure, one of the most strategically important chokepoints on the planet.

After the U.S. and Israel conducted coordinated strikes on Iranian targets over the weekend, the big question became: does this spill over into shipping? Because if tankers start rerouting, or if insurance costs spike, or if Iran retaliates by disrupting traffic through the strait—you don’t even need an actual supply disruption to send energy prices surging.

Just the possibility is enough. And we saw that play out in real time.

WTI crude oil spiked to nearly $120 a barrel on Monday morning before pulling back sharply after President Trump told CBS News that the military operation is nearly complete.³ Brent crude settled around $94, up roughly 50% from the start of the year according to the EIA’s latest short-term outlook.³

When energy prices spike like that, the effects don’t stay contained to gas stations. Higher oil feeds into transportation costs, which feeds into food prices, which feeds into manufacturing inputs, which feeds into basically everything. A common rule of thumb: every $20 increase in oil adds roughly $0.50 per gallon at the pump. Multiply that across a household’s annual fuel consumption and the broader inflation ripple, and you’re talking about real money.

The Jobs Report Made Things Worse

On Friday, the Bureau of Labor Statistics reported that the U.S. economy lost 92,000 jobs in February.⁴

Economists were expecting a gain of roughly 50,000.

That’s not just a miss—it’s a reversal. And the revisions made it even uglier: December was revised from a gain of 48,000 to a loss of 17,000. January was revised down slightly to 126,000.⁴

Now, some important context. A big chunk of February’s losses came from healthcare, which shed 28,000 jobs largely because of a Kaiser Permanente strike in California and Hawaii that pulled more than 30,000 workers off payrolls during the BLS survey week.⁴ That strike has since been resolved, so some of that should bounce back in March. Federal government employment also continued to decline, down another 10,000 for the month—part of a broader reduction of 330,000 federal jobs since late 2024.⁴

But even with those caveats, the trend is concerning. This was the third time in the past five months that payrolls declined. The economy has averaged fewer than 5,000 new jobs per month since January 2025.

The Fed Is Trapped

So now you’ve got oil prices threatening to reignite inflation and a labor market that’s weakening at the same time. That combination has a name: stagflation. And it’s basically the worst-case scenario for central bankers.

The Federal Reserve currently has rates at 4.50–4.75%. Markets are pricing in the possibility of two to three rate cuts later this year. But here’s the problem: if they cut rates to support the economy, they risk pouring gasoline on an inflation fire that oil prices are already stoking. If they hold rates where they are, they risk watching the labor market deteriorate further.

There’s no clean answer. And that uncertainty is exactly what’s driving the volatility.

The Breakdown

Target Date Funds: The Autopilot Portfolio

Let’s talk about something that sits inside millions of retirement accounts that most people never fully look into.

Target date funds.

If you’ve ever logged into your 401(k) and seen something like “Target Retirement 2040” or “Target Retirement 2055”—those are target date funds.

The concept is straightforward. You pick the fund that matches roughly when you plan to retire. The fund manager handles the rest.

When retirement is decades away, the fund holds more stocks—because stocks have historically produced higher long-term returns, and you have time to ride out the dips. As you get closer to retirement, the fund gradually moves into bonds and more stable investments to protect what you’ve built. This gradual transition is called the “glide path.”

You don’t have to rebalance anything yourself. You don’t have to decide when to move out of stocks. You don’t have to panic-sell during a downturn and try to time your way back in.

That last part matters more than people think. The single biggest mistake most investors make isn’t picking the wrong fund. It’s panicking and changing their strategy at exactly the wrong moment. Target date funds are designed to take that impulse off the table.

Now, they’re not flawless. Different fund companies design their glide paths differently—some are more aggressive, some more conservative. And fees vary, so it’s worth checking what you’re paying. But for a long-term investor who doesn’t want to spend their weekends researching portfolio allocation models, a target date fund can be a genuinely solid foundation.

Not everything in investing needs to be complicated. Sometimes the smartest move is building something that runs in the background while you live your life.

The Property Playbook

Welcome to a new recurring section of Invested in Us. Each week, we’ll break down a concept, strategy, or trend in real estate investing —because real estate is one of the most powerful wealth-building tools in the world, and most people only know the surface level.

How the Biggest Investors in the World Think About Real Estate

When most people think “real estate investing,” they think of buying a house or maybe an apartment building. That’s real estate. But it’s one slice of a much bigger picture.

Institutional investors—the pension funds, endowments, and sovereign wealth funds managing hundreds of billions of dollars—look at real estate as a collection of specialized sectors, each with completely different risk profiles, return characteristics, and economic drivers.

The major sectors most people know: residential (apartments, single-family rentals, manufactured housing), office (corporate buildings), retail (shopping centers, malls), and hospitality (hotels, resorts).

But the sectors that have been growing fastest are the ones most people never think about: senior housing, data centers, and self-storage facilities. Data centers alone have become one of the most in-demand property types on the planet as artificial intelligence and cloud computing have exploded. Senior housing is being driven by demographics that are basically locked in for the next 20 years.

Each of these sectors responds differently to economic conditions. When oil prices spike and inflation rises—like right now—some real estate sectors get squeezed while others actually benefit from the pricing power that comes with essential services. Knowing the difference is what separates professional capital allocation from guessing.

We’ll go deeper on individual sectors in future issues. For now, the takeaway is this: real estate is not one thing. And the more you understand about how institutional money thinks about it, the better positioned you are to make smart decisions with your own.

Closing Thoughts

Here’s what stood out to me this week.

In the span of a few days, oil went from $80 to nearly $120 and back down again. The jobs report swung from an expected gain to an actual loss. Markets went from “cautiously optimistic” to “genuinely scared” and then partially recovered—all before most people finished their Monday morning coffee.

The speed of it is the story.

We live in a world where a shipping lane most people have never heard of can directly affect what you pay for gas and groceries next month. Where a strike at one hospital system in California can move a national employment number. Where a comment from a president on a phone interview can swing oil prices $20 in an hour.

None of that means you need to react to every headline. It means the opposite, actually. The people who did best last week were the ones who already had a plan—who weren’t scrambling to figure out what their portfolio looked like after the news broke.

That’s what financial planning is really for. Not predicting the future. Surviving it.

If this week is making you think more seriously about your financial plan, we’d love to talk.

→ Schedule a call with NJK Wealth Management

We’re teaching money the way it should’ve been taught to us. If this issue helped you understand what’s happening, share it with someone who could use it.

If you’re learning and enjoying the content, please like, share, comment, or repost. Thanks family!