The S&P 500 Energy Sector Is Up 25% This Year. Growth Stocks Are Lagging. And Most People Have No Idea Why.

Invested In Us | Issue 16 | March 2, 2026

Markets dipped about half a percent last week. The S&P 500 is still up around 0.7% year-to-date. If you only looked at those numbers, you’d think nothing interesting is happening. You’d be wrong.

State of Capital — What’s Actually Happening

Here’s what most people are missing right now: the market isn’t just moving, it’s rotating.

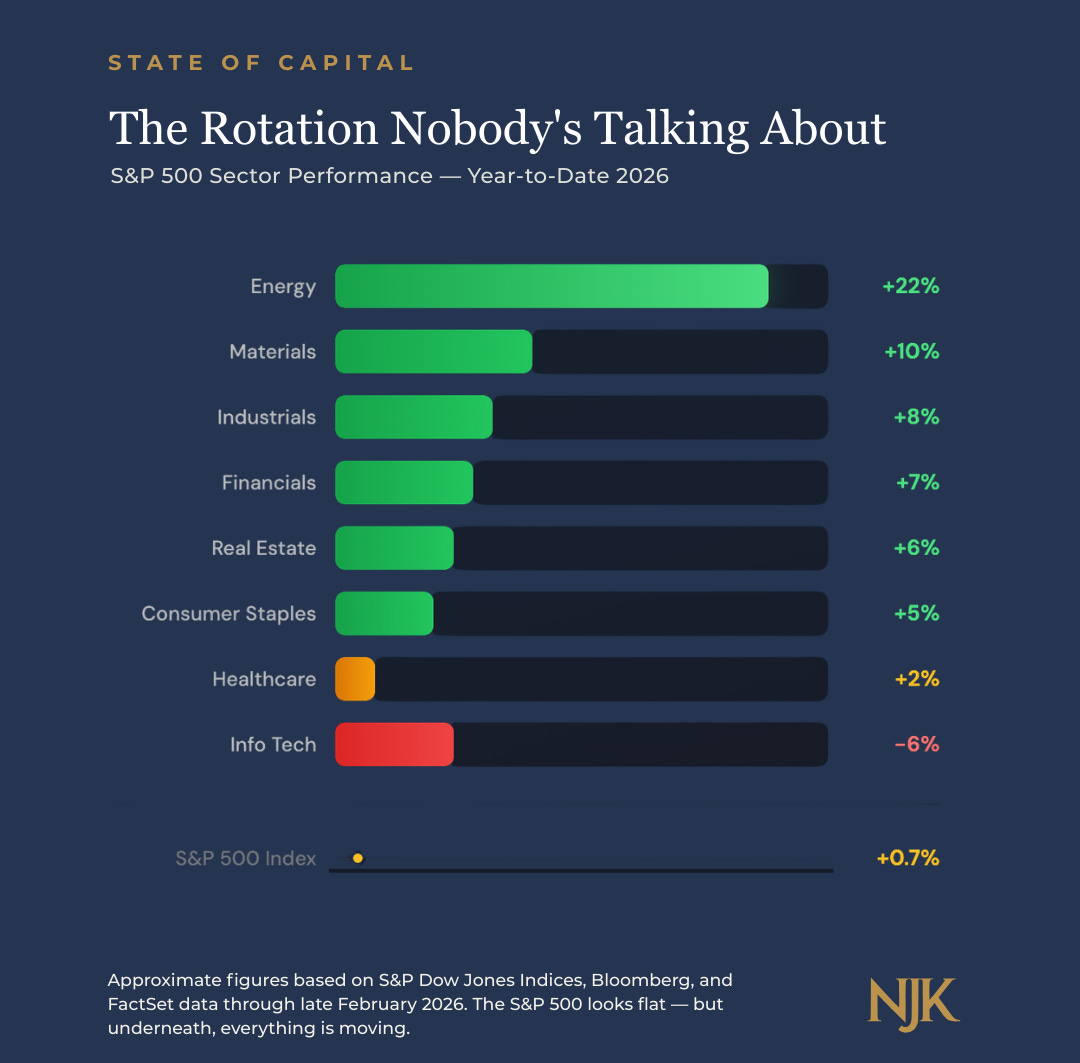

The S&P 500 Energy sector is up more than 25% year-to-date. That’s not a small move. That’s a massive repricing of an entire sector. And energy isn’t the only one running: materials, industrials, consumer staples, real estate, and financials have all been putting up strong numbers too.

Meanwhile, the growth names that dominated your timeline for the last few years? They’re lagging. Value is beating growth. And here’s the part that might surprise you even more: U.S. stocks are trailing international markets. European and Asian equities have been stronger on a year-to-date basis.

So what does all of this tell us?

That nobody (no matter how confident they sound on a podcast) knows ahead of time which sector or which region is going to lead in any given year. If your portfolio is concentrated in one area, you feel the rotation fast. Diversification sounds boring until it’s the reason you’re still sleeping at night.

On the bond side, the 10-year Treasury yield dropped below 4% for the first time in a while. If you’ve been wondering why mortgage rates, auto loans, and credit card rates have come down slightly, that’s the reason.

Corporate earnings were strong in Q4 and throughout 2025. The global economy is still on solid footing.

The real issue right now isn’t weakness. It’s that nobody knows what’s coming next. And that uncertainty is showing up everywhere.

Policy & Economics

Why Energy Is Back in the Spotlight

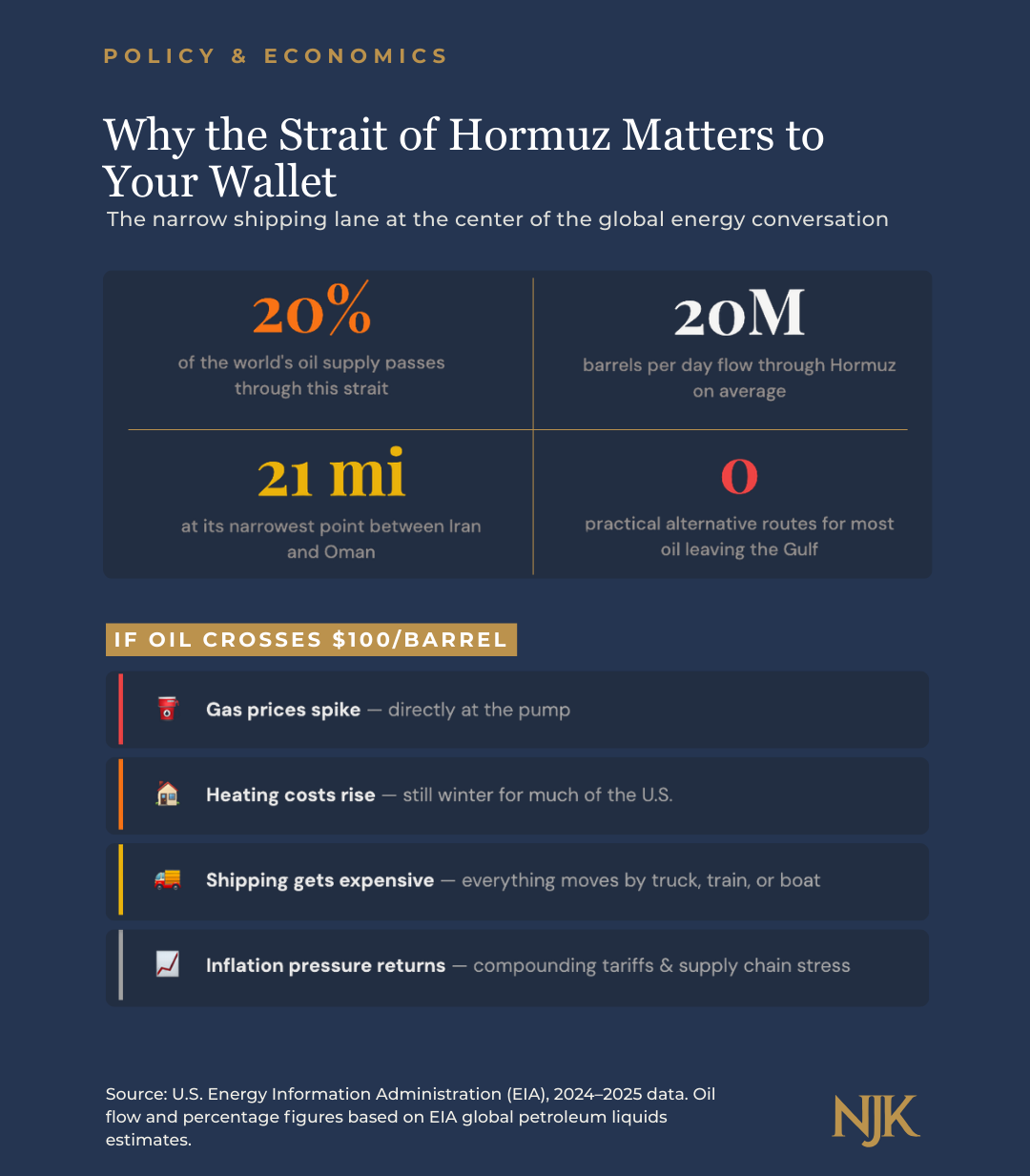

Over the weekend, things got real. The United States and Israel conducted coordinated strikes on Iran. Markets reacted immediately, especially in the energy space.

The big concern here is the Strait of Hormuz. It’s a narrow shipping lane, and roughly 20% of the world’s oil supply passes through it. With tensions rising, shipping captains have already started rerouting vessels. Insurance companies are reconsidering coverage for ships in the region.

And that alone can push prices higher—even before there’s an actual supply disruption.

If oil crosses $100 per barrel, the ripple effects hit fast. Higher gas prices at the pump. Increased heating costs (and we’re still in winter). More expensive transportation for goods. And renewed inflation pressure across the board.

Keep in mind: almost everything you buy gets to you by truck, train, or boat. In a world already dealing with tariffs, lingering post-COVID inflation, and fragile supply chains, an energy shock amplifies everything.

This is exactly why real assets have been attracting capital lately. Energy, gold, silver, real estate, infrastructure, commodities have been rallying not just because demand is up, but because investors are hedging against uncertainty. When people don’t know what’s coming, they tend to move toward things they can see and touch.

The Breakdown

How Retirement Accounts Can Lower Your Tax Bill Today

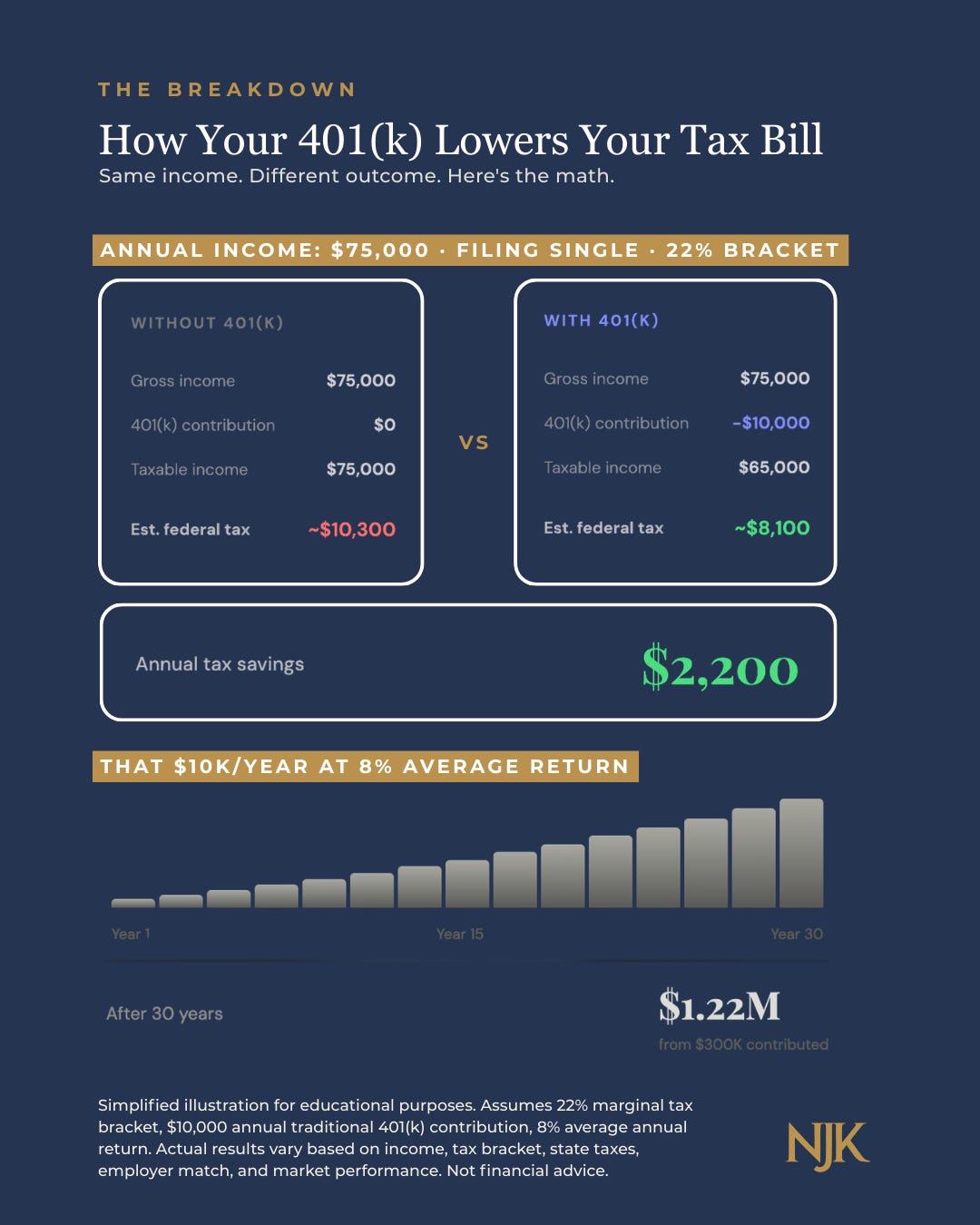

Let’s talk about one of the most underused tax strategies out there. It’s not complicated. It’s not some loophole. It’s just... using your retirement accounts the way they were designed.

When you contribute to a traditional 401(k) or IRA, that money comes off your taxable income for the year. Meaning you could owe less in taxes right now while also building toward your future.

So you’re lowering your tax bill today and giving your money time to grow and compound over decades. That compounding piece is where real wealth gets built. Not overnight. Not from one hot stock. From time.

Now, there’s a tradeoff. This money is meant for retirement. If you pull it out early, you’ll likely face penalties and taxes. So don’t put money in here that you might need next year for rent or a car repair.

But for long-term savings? We’re big fans of these accounts.

They create discipline. They reduce your taxable income. And they let your investments grow without getting eaten alive by taxes every year.

None of that is flashy. Nobody is making viral content about maxing out a 401(k). But it works. And the people who start early and stay consistent are the ones who end up with real options later in life.

The Conversation

Keep It Simple

Weeks like this are a good reminder of something we come back to a lot:

We don’t control geopolitics.

We don’t control where the market rotates next.

We definitely don’t control whether international stocks outperform domestic ones.

What we do control is whether we stay disciplined when things get noisy.

Staying diversified. Rebalancing when the numbers call for it. And making decisions based on your actual goals instead of whatever headline is trending.

Markets will always move. That’s what they do. A well-structured plan is built to move with them, not react to every tremor.

Closing Thought

Every week there’s a new reason to second-guess your plan. This week it’s Iran and oil prices. Next week it might be tensions in Cuba or something else. The noise never stops.

But here’s what we keep coming back to: the basics work. Diversify. Use your retirement accounts. Don’t try to outsmart the market on a Tuesday afternoon because of a headline. The boring stuff is boring because it works slowly. And slow is how real wealth actually gets built.